.png)

Alberta’s power market in 2025 has been defined by a weird combo: more hours that feel “too cheap to meter,” and enough peaks to remind everyone this is still Alberta.

Midday is increasingly where the lowest prices show up; zero-dollar hours are shifting from classic overnight off-peak into the afternoon as wind and solar peak. At the same time, late-day and evening 'stress' hours still produce outsized volatility when demand stays high and solar drops off.

That split is now a core strategic problem, net position management, hedging, and dispatch planning can’t rely on simple “peak vs off-peak” intuition when the curve keeps flipping it's shape, and when the lowest-cost blocks are pushing record territory (for example, the daily lowest-cost eight hours averaging CAD 10.93/MWh in August)

Reliability and demand growth sit underneath all of it. Alberta saw materially higher Energy Emergency Alert (EEA) activity through 2022–2024, and while the first half of 2025 had no EEA events, the drivers of future grid stress are not subtle: electrification and new large loads (including data centres) are explicitly flagged as demand growth forces.

AESO’s long-term planning has already shifted in response. Its load growth outlook increased from 0.4% to 1.2% per year, and the reference case shows Alberta Internal Load (AIL) increasing meaningfully over time (26% from 2024 to 2043). In practical terms, the market is being asked to absorb higher demand variability while the supply stack becomes more weather-shaped.

And then there’s the rules. Alberta is in the runway period for the Restructured Energy Market (REM), which introduces nodal pricing (LMP), SCED, co-optimization of energy and a 30-minute ramping product (R30), and a different scarcity and settlement framework.

Implementation isn’t tomorrow, but it’s not “someday” either. Stakeholder consultations are expected in late 2025 with implementation targeted for mid-2027. That timing matters for 2025 decision-making: the choices you make now around siting, flexibility, hedging logic, and operations are increasingly about preparing for a market where location and ramp capability show up directly in price.

This outlook breaks 2025 into the regimes that drive outcomes (cheap-hour self-utilization vs scarcity-hour volatility), connects those regimes to forecasting and net position risk, and then pulls the thread forward into what REM will reward and punish. The goal is to give operators, traders, asset owners, and exec teams a decision-grade read on what’s changing, and what to adjust before 2025 turns into the “last easy year.”

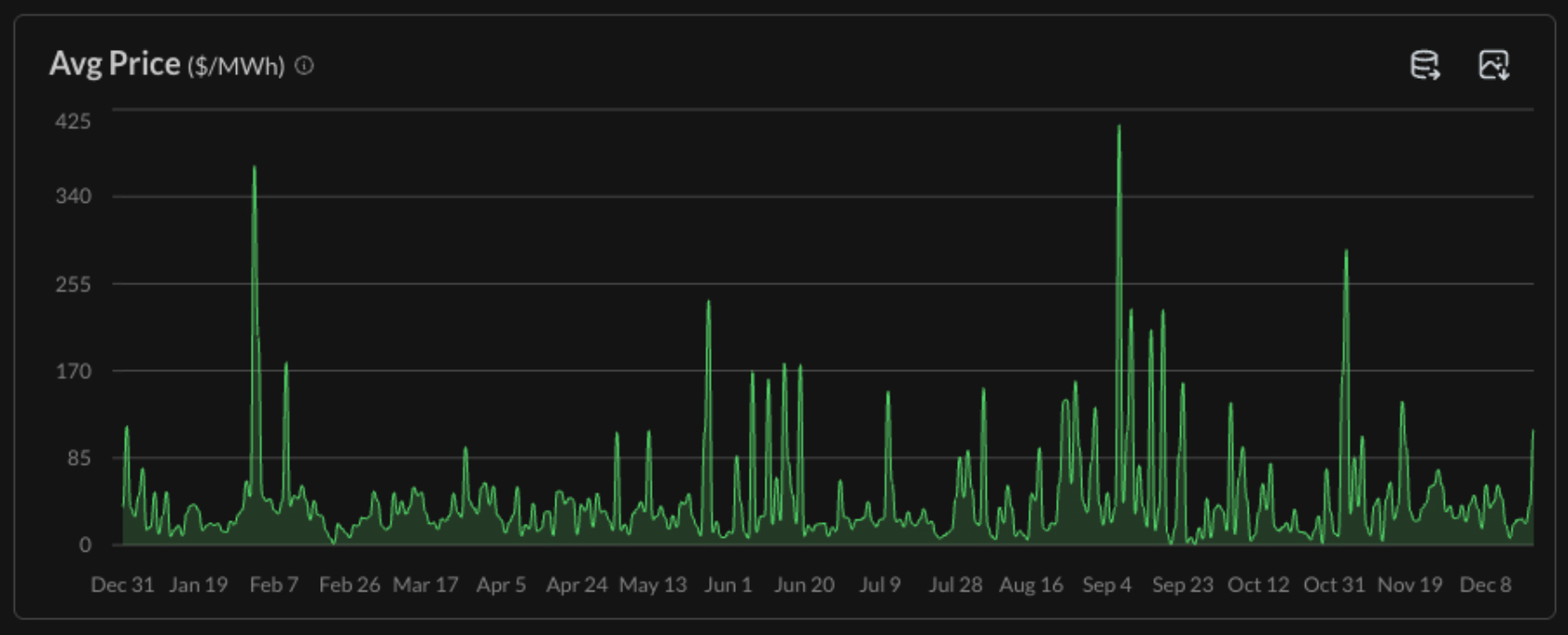

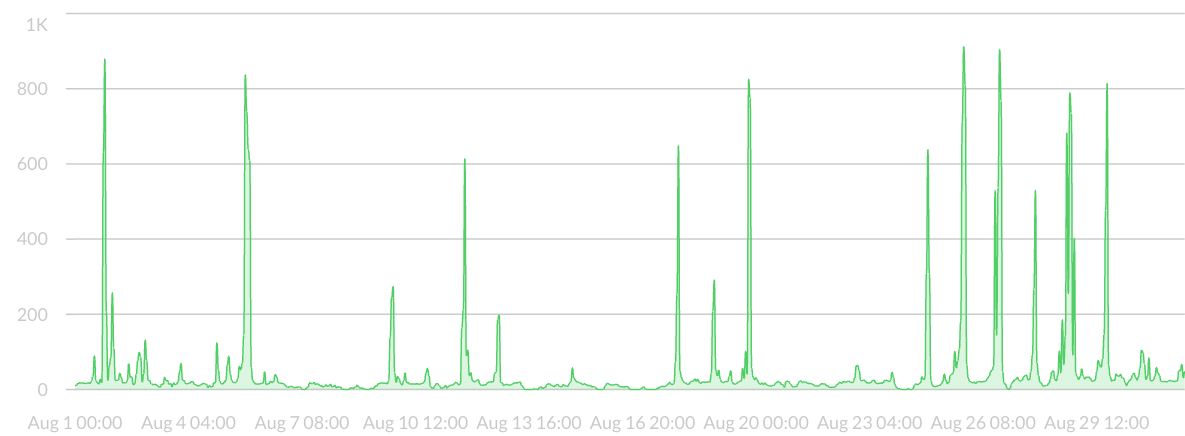

Arcus data and public market reports show Alberta’s price distribution remains heavy‑tailed. For most hours, prices stay in a low band, but a handful of hours each month carry the bulk of the value and risk. The Alberta Market Surveillance Administrator (MSA) Q2 2025 report notes that average pool price in the second quarter was CAD 40.48/MWh, down 10% from Q2 2024, but this average concealed extremes: on 17 June two Genesee units tripped offline, reducing supply by 881 MW; contingency reserves were fully deployed and the System Marginal Price (SMP) hit the CAD 999.99/MWh offer cap. Similar spikes occurred on 8 June when multiple gas units failed, again clearing the price at the cap.

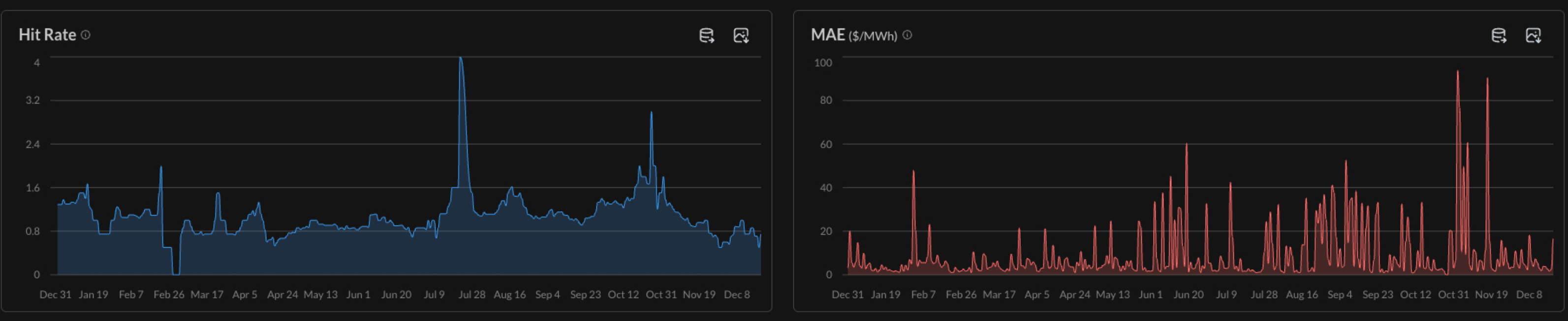

These rare but dramatic events align with Arcus error spikes. For long stretches the forecast tracks prices closely, but during the biggest price jumps, especially late in the year – absolute errors and normalized errors rise sharply. The implication is that average error metrics hide tail risk. RMSE is much higher than MAE, indicating that large misses dominate the squared error; this matches the reality that a handful of hours drive profitability.

The year also saw unprecedented low prices. An August 2025 snapshot shows that while ultra‑low prices (CAD 0.01‑30/MWh) were common, there were still evenings with extreme highs. Average pool price for August was CAD 50.35/MWh, 47% higher than August 2024 yet still moderate for a traditionally volatile month. The striking trend is in the bottom end of the distribution: the average of the daily lowest‑cost eight hours reached CAD 10.93/MWh, the lowest level in at least two decades. Zero‑dollar hours also shifted from overnight to afternoons when solar and wind production peaked.

This structural change matters for net position management. Participants with flexible load or storage who can shift consumption to low‑price hours can capture significant savings. Arcus savings metrics show meaningful benefits for those who react to price patterns, though the gap between perfect savings and realized savings remains; this gap increases during periods when forecasts or availability (downtime) miss the lowest‑price windows.

For the first time, April 2025 saw off‑peak prices exceed peak prices. High thermal availability and strong solar generation flattened the supply curve, reducing volatility in the daytime but pushing off‑peak prices higher. This inversion signals that traditional definitions of “peak” and “off‑peak” are less useful; traders and procurement teams must monitor intraday curves, not just daily averages.

Forecasters often report statistics like Mean Absolute Error (MAE), Mean Absolute Percentage Error (MAPE) and Root Mean Square Error (RMSE). A recent paper on short‑term load forecasting notes that MAPE is scale‑independent and interpretable as a percentage, making it useful for comparing across datasets, whereas MAE expresses error in the same units as the data and is more robust to outliers.

Optimising solely for MAPE can bias forecasts toward underestimating demand; optimising MAE tends to balance errors but may understate rare spikes. The paper proposes evaluating not just average MAPE/MAE, but the frequency with which errors exceed defined thresholds, a concept Arcus also implements through confusion‑matrix and threshold metrics.

Arcus metrics indicate MAE around CAD 8.9/MWh with RMSE about CAD 15.6/MWh. Because RMSE penalizes large errors more heavily than MAE, the gap shows tail events dominate the squared error. Normalized MAE climbs steadily from mid‑year and peaks late in the year, highlighting performance drift.

Precision, recall and F1 scores deteriorated mid‑year and late‑year. This suggests the model performs best in stable regimes and struggles during structural changes – for instance, when ramping reserves are constrained or when renewable output is less predictable due to weather.

These patterns echo academic research: in a case study of industrial consumers, day‑ahead forecasts struggled during holidays because consumption patterns changed sharply. It set MAPE thresholds of 20% for day‑ahead forecasts and applied a fused model to improve performance, especially during special periods.

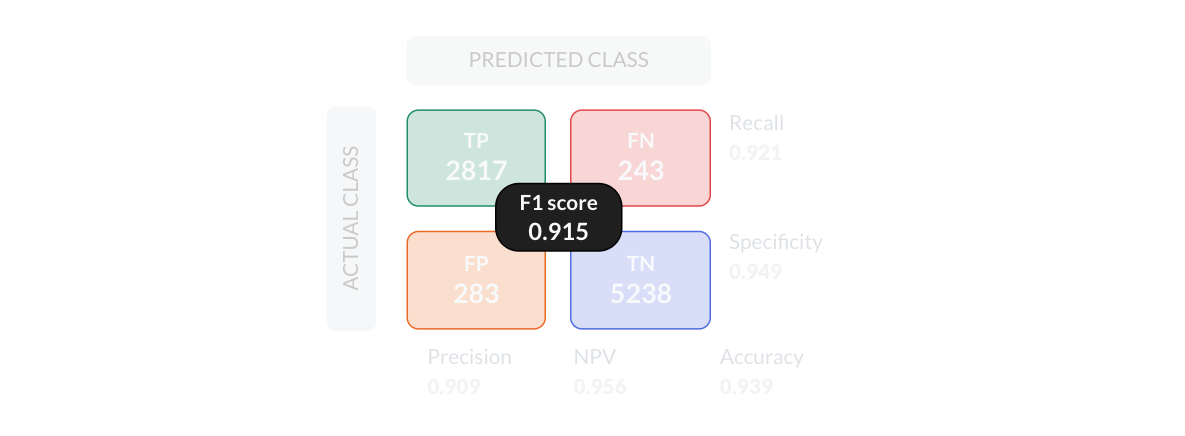

Arcus reports 440 hours of downtime year‑to‑date, yet a capture rate of 99% (based on specific threshold and other considered parametes).

Regardless, downtime in the wrong hours can negate accuracy gains. For example, the difference between perfect profit and realised profit is low, suggesting downtime had a bigger impact on savings opportunities than on profit, perhaps because savings opportunities often occur during low‑price hours when the system might be offline.

Reliability is not just a technical concern; it has immediate commercial consequences. The Canada Energy Regulator (CER) notes that Energy Emergency Alerts (EEAs) – NERC’s classifications for serious grid events – increased sharply in Alberta, with four EEA 2 and seven EEA 3 events in 2022. The first half of 2025 had no EEAs, but these recent spikes show the system is operating closer to its limits.

Extreme weather has already tested the grid, during a cold snap in January 2024, Alberta narrowly avoided rolling blackouts when import transmission lines were constrained. March 2025 brought an ice storm in Ontario that left over a million customers without power, showing the importance of resilience.

The CER report points out that electricity demand is expected to rise significantly due to decarbonisation, electrification of transportation and buildings, and the emergence of data centres. This matches the 2024 Long‑Term Outlook (LTO), which revised Alberta’s load growth from 0.4% to 1.2% per year and noted that data centres and AI workloads are major drivers. Even under the reference case, average hourly Alberta Internal Load (AIL) is expected to increase by 26% between 2024 and 2043, while the high‑electrification scenario sees a 44% increase.

High penetration of variable renewable energy sources (VRES) introduces volatility. The CER highlights that VRES must be managed carefully due to their intermittency. Supply diversification is crucial: combining VRES with battery storage and dispatchable resources allows excess generation to be stored and released when needed. Transmission expansion and demand response also play roles. However, modernisation introduces new vulnerabilities (cyber and physical) that must be addressed.

Alberta operates an ancillary service market for operating reserves, which include regulating reserves (minute‑to‑minute balancing) and spinning/supplemental reserves (ten‑minute contingency). Providers submit competitive bids and receive availability payments, earning upwards of CAD 240,000 per MW annually. This service runs 24/7 and becomes more lucrative during winter and on‑peak hours.

A reliability roadmap acknowledges that more intermittent generation and fast‑ramping loads require flexible resources. It calls for real‑time stability assessments, increased regulating reserve procurement, 30‑minute ramping product (R30), and Fast Frequency Response (FFR) services. The AESO proposes to procure up to 750 MW of highly available FFR+ to support 800 MW import on the BC intertie and 300 MW on the Montana intertie.

The reliability roadmap also highlights low system strength due to the retirement of synchronous generators and the rise of grid‑following inverters, particularly in regions like Medicine Hat and Pincher Creek. Low system strength leads to voltage fluctuations and reliability risks. The AESO plans to procure grid‑forming inverters, implement performance‑based rules for frequency response, and calibrate intertie limits to manage system strength.

Alberta’s current market uses a single system marginal price (SMP) that ignores congestion. The REM introduces locational marginal pricing (LMP) and a security‑constrained economic dispatch (SCED). Energy and a new 30‑minute ramping reserve (R30) are co‑optimised; prices will reflect the cost of meeting demand at specific nodes. Scarcity pricing is embedded through an escalating price cap that rises from CAD 1000/MWh to CAD 3,000/MWh by 2032 and a negative price floor dropping to CAD 100/MWh. This structure sends stronger investment signals for flexible, dispatchable resources.

The REM creates new products: the R30 ramping reserve to ensure enough flexible capacity for sudden changes, and the Reliability Unit Commitment (RUC) to commit resources that might not otherwise be economic in the energy market. These resources will be compensated, ensuring they remain available for reliability without relying on out‑of‑market directives.

To balance investment signals with consumer protection, the REM introduces broad and local market power mitigation frameworks. A secondary offer price cap limits price manipulation but still allows scarcity pricing. Settlement intervals will shift to five minutes, aligning financial settlement with dispatch and pricing; cost allocation will better reflect causation.

The REM adopts an Optimal Transmission Plan (OTP) framework that evaluates new projects based on reliability needs, legislation or net benefits (cost–benefit analysis). This replaces the zero‑congestion transmission expansion model. Stakeholder consultations on ISO rules will occur in late 2025, with implementation targeted for mid‑2027. Participants need to prepare now: nodal price signals will reward siting near load or strong interties and penalize congested regions.

The AESO’s 2025 Transmission Rate Outlook (TRO) projects significant capital spending on system expansions, connection projects, and maintenance. Forecast assumptions include updated cost and schedule estimates for transmission projects, recovery of project costs over 30‑60 years, forecasted energy requirements, inflation and ancillary services costs. As a result, the average transmission rate is expected to rise from CAD 43/MWh in 2025 to CAD 57/MWh by 2034, while the average residential bill (600 kWh/month) increases from CAD 25 to CAD 33. By 2030, residential customers are forecast to pay about CAD 29/month in transmission charges.

The 2024 LTO notes that load growth expectations have tripled: from 0.4% to 1.2% per year, driven by macroeconomic factors, electrification and new load connection projects. Alberta remains a winter‑peaking grid; electrification of heating and EVs creates acute ramps that coincide with distributed solar decline. By 2030, renewable capacity (wind, solar, hydro, biomass) is expected to exceed peak demand, and renewable generation could supply 30% of electricity.

Dispatchable natural gas will remain the dominant firm capacity, with continued growth in energy storage; scenarios include decarbonized baseload (CCUS, small modular reactors) and high electrification.

Imports and exports play a growing role. The MSA reports that the BC and Montana interties tripped four times in Q2 2025, causing frequency deviations and requiring support from Alberta generators. The FFR+ procurement aims to increase import capability on these interties by ensuring fast frequency response. The LTO assumes that expanded intertie capacity will double current import capability in high‑electrification scenarios.

Arcus metrics show that net revenue differences between perfect and realized strategies are small on the profit side but larger on the savings side. In a heavy‑tailed market, missing or misclassifying a handful of events (false negatives) can erase months of steady performance. Participants must measure and manage their net position – the difference between contracted supply and actual load – at a granular level. High precision and recall reduce unnecessary hedges (false positives) and missed opportunities (false negatives). Real‑time dashboards and alerts should flag forecast drift and system outages.

Flexible assets, fast‑ramping gas, battery storage, demand response – are becoming the primary hedge against price spikes and reliability events. The REM’s scarcity pricing will reward such flexibility. Investment decisions should consider not just average earnings but the ability to monetize extreme hours. Storage developers should model both positive and negative price scenarios given the introduction of a CAD 100/MWh floor.

Alberta’s power market stands at an inflection point. The 2025 outlook is not simply an extrapolation of recent averages. It is shaped by heavy‑tail price distributions, growing demand from electrification and data centres, increasing variable renewable generation, and the transition to a nodal market with new reliability products. Forecasting models must evolve from static error minimization to dynamic risk management. Operational reliability- through robust operating reserves, FFR+, and grid‑forming inverters – must accompany the shift to cleaner generation. Policy frameworks like the REM will rewire incentives, making location, flexibility and responsiveness central to commercial success.

Explore our solutions to unlock market opportunities and manage risks effectively.

Get Started

Shifting Assets For Data Center Energy Management

Arcus Power Announces Patrick Smith as VP of Technology to Accelerate AI Energy Innovation

Breaking down how Arcus’s high-probability approach made capturing IESO GA peaks possible